A brief look at the banking inquiry

Sean Laidlaw

This week we sat down and read the Finance and Expenditure Committee Inquiry into Banking Competition. While it is positive to see the government taking a more active role in improving New Zealand’s very limited banking system, the recommendations for the Agricultural sector provided some disappointing reading. New Zealand’s Agricultural lending stands at around NZD $61 billion and with far from transparent pricing across the market, this interest cost is preventing farmers and the sector from better capital efficiencies, and improved production.

So, what were the Committee Recommendations?

- Cease capital increases for banks

..recommendation that, effective immediately, the Reserve Bank cease the planned incremental increases to capital requirements. - Review rural requirements

..recommend the Reserve Bank review the capital requirements for rural lending and that any changes are monitored and publicly reported on. - Formal disclosure of factors

..recommend agricultural lenders formally disclose to customers the specific factors they consider when calculating their risk margin and pricing.

While these recommendations are very positive for the sector, do they do enough to make banking competition more viable in New Zealand?

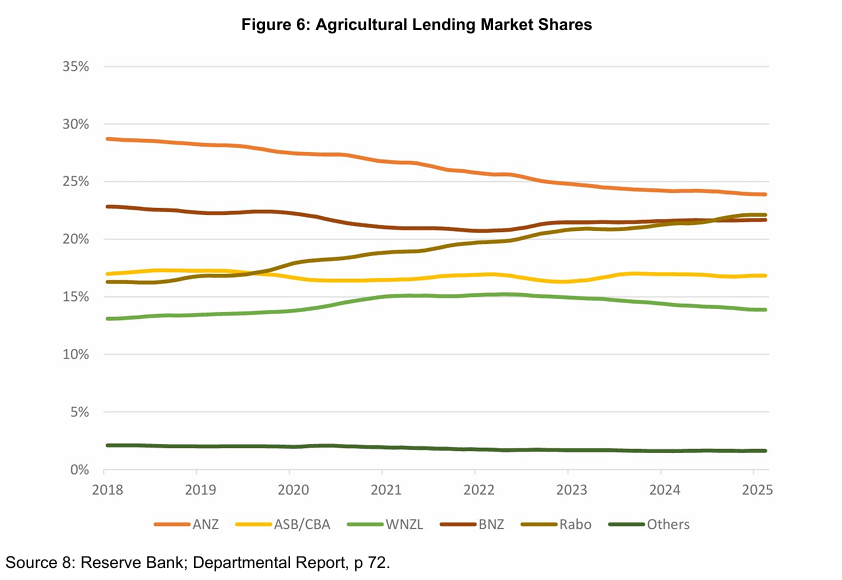

Same old Bad Guys

The much discussed “Big 4” Australian-owned banks ANZ, ASB, BNZ, Westpac still hold around 80 percent of Agri-lending, but Rabobank has steadily gained market share over the past six years, largely at ANZ’s expense.

Kiwibank, currently majority shareholder owner by the New Zealand Government currently does not participate in rural lending. Its impending capital raise of $500 Million NZD would have no immediate impact on the Agri lending sector.

While it is easy to beat up on the banks, they only operate within the legislation and markets that consumers and politicians provide them, unless we’re asking these questions around how we make the sector more competitive, then we will never see change. Reductions in capital requirements, particularly for smaller lending organisations, will allow new market participants the ability to enter the market and improve the sectors optionality, we have spoken to several companies looking at how a lending provider could better serve the New Zealand Agri sector and are looking forward to improvements in the competitive landscape, even if for partial loan portfolios or product specific lending.

Opaque Pricing

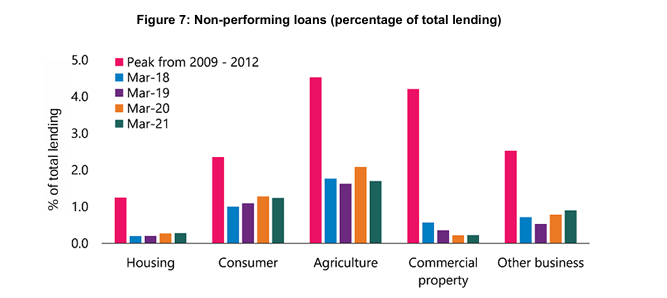

Would the New Zealand population accept the same pricing model in residential lending as it allows in Agricultural lending? Lenders view agricultural loans as higher risk than residential mortgages, driven by commodity-price volatility and the complexity of farm cash flows and it’s easy to accept that the sector might need to incur some level of risk pricing, and when we look at the face value graphs provided by the committee report you would tend to agree.

However, what this graph doesn’t show is that from 2008 – 2009, growth across Agricultural lending topped out at 22% annually in ‘09 driven largely because of the 07/08 bumper season in Milk prices, so while housing and banks grappled with the fall out of the GFC, banks decided Agriculture was a lower risk?

The definition of non-performing, which is listed as default because the borrower has missed scheduled payments for a defined period (typically 90 or 180 days), can also create room for mis-categorisation amongst farmers who operate to 6 monthly or annual income cycles.

The committee report mentions that the typical two-year farm loan rates run about 170 basis points above residential mortgages; while only around 60 basis points of that spread is attributable to capital requirements, with the rest covering operating costs, expected losses, and profit margins. In simple terms, despite rural branches closing, Agri lending teams getting smaller and more centralised around the country and the days of your banker coming to see you on farm getting fewer, the banks believe your Farm loan still costs them more than an Auckland home loan.

Improving the transparency in which pricing is disclosed will allow New Zealand farmers to better compare products as well as outcomes. It will also allow for accountants, advisors and the wider industry to identify where capital access is prohibitive.

With the impending succession wave across New Zealand’s Agricultural sector, the decisions and actions because of this Inquiry will be vital for setting up the Next generation of farmers up for success into the future. While the recommendations are a great start, we need to ensure they go far enough.